TL;DR:

- Your credit score greatly influences car loan eligibility, interest rates, and total ownership costs.

- A higher score allows access to better rates and more favorable loan terms, saving money over time.

Your credit score is the single most powerful factor determining whether you get a car loan, at what interest rate, and on what terms. Lenders use it to measure risk before approving any auto financing. Borrowers with scores of 661 or higher secured 68.4% of all retail vehicle financing in 2026, while those with scores at or below 600 captured only 15.8%. That gap tells you everything about the role of credit score in car buying. The higher your score, the more lenders compete for your business. The lower it sits, the more you pay for the privilege of borrowing.

How does your credit score affect auto loan rates and terms?

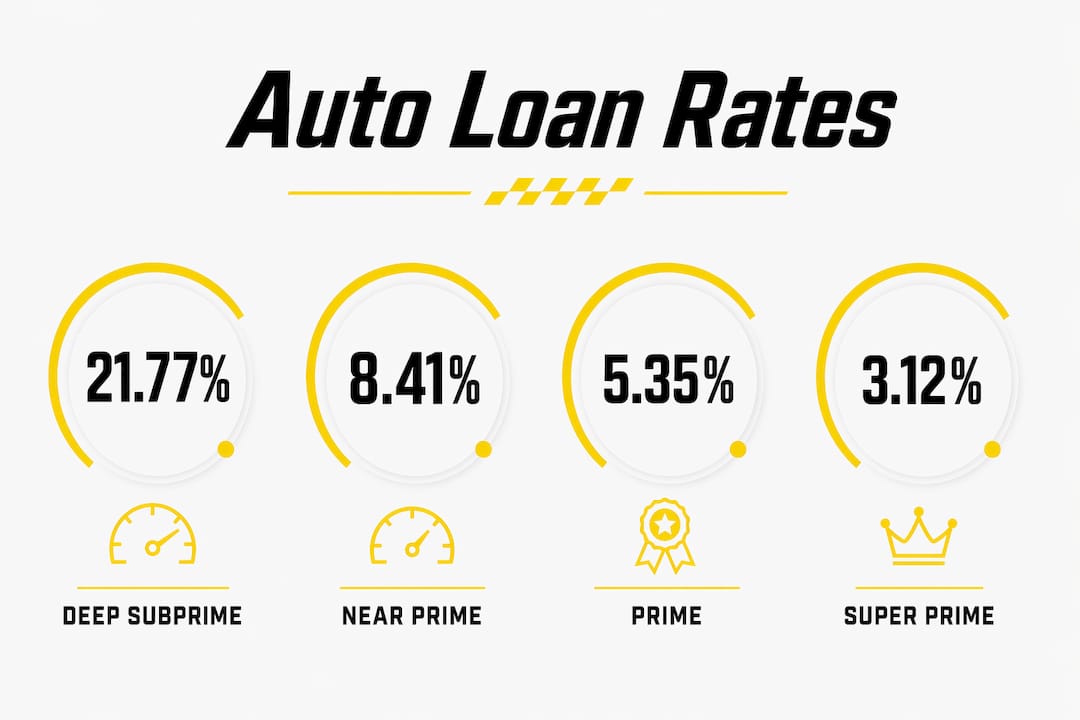

Your credit score places you in a lending tier, and that tier sets your interest rate. Lenders group borrowers into five categories: super prime, prime, near prime, subprime, and deep subprime. Each tier carries a different rate range, and the difference between the top and bottom is dramatic.

Deep subprime borrowers with scores between 300 and 500 faced average interest rates as high as 21.77% on car loans in Q1 2026. That rate is not a penalty. It reflects the statistical likelihood that a lender will not be repaid. Meanwhile, the national average for new car loans sat at 6.37% and used car loans at 11.26% as of late 2025. Those averages blend all tiers together, so your personal rate depends entirely on where your score lands.

Higher rates do more than raise your monthly payment. They inflate the total cost of the vehicle over the life of the loan. A buyer financing $30,000 at 6% pays far less than a buyer financing the same amount at 18%, even if both drive off the same lot on the same day.

| Credit tier | Score range | Typical new car rate | Typical used car rate |

|---|---|---|---|

| Super prime | 781–850 | ~5% or lower | ~7% |

| Prime | 661–780 | ~6–8% | ~9–11% |

| Near prime | 601–660 | ~9–12% | ~13–15% |

| Subprime | 501–600 | ~13–18% | ~18–21% |

| Deep subprime | 300–500 | ~19–21.77% | ~21–22%+ |

Rate ranges are approximate and vary by lender, loan term, and market conditions.

Pro Tip: Get your credit report from all three major bureaus, Equifax, Experian, and TransUnion, before you apply for any auto loan. Errors on one report can drag your score down without your knowledge.

- A lower credit tier typically requires a larger down payment to offset lender risk.

- Loan terms for subprime borrowers are often shorter, which raises monthly payments further.

- Some lenders cap loan amounts for buyers below a certain score threshold.

What is the FICO Auto Score and why does it matter?

Most buyers check their base FICO Score or VantageScore and assume that is what lenders see. That assumption is wrong. The FICO Auto Score is a specialized model built specifically to predict the likelihood of missing a car payment. It runs on a 250–900 scale, not the standard 300–850 range used by base FICO models.

The FICO Auto Score places more weight on your history with installment loans, particularly past auto loans. If you paid off a previous car loan on time, that history boosts your FICO Auto Score more than it would boost your base score. The reverse is also true. A missed car payment in your history hits harder on the FICO Auto Score than on a general credit model.

Lenders vary in which FICO version they use, and the same positive credit behaviors that raise your base FICO score typically improve your FICO Auto Score as well. Paying bills on time, keeping credit card balances low, and avoiding new credit applications all move both scores in the right direction. The FICO Auto Score is widely adopted across the auto lending industry and is considered the most predictive metric for missed car payments.

Pro Tip: Ask your lender directly which FICO version they pull. Some use FICO Auto Score 8, others use version 9. Knowing this helps you understand why your lender’s view of your credit may differ from what you see on a free monitoring app.

Key differences between the FICO Auto Score and base FICO models:

- Scale: 250–900 versus 300–850

- Greater weight on auto loan and installment debt payment history

- Used primarily by auto lenders, not mortgage or credit card issuers

- Free credit monitoring tools rarely show your FICO Auto Score

What are your financing options with different credit scores?

No universal minimum credit score exists for buying a car. Lenders set their own thresholds, and the auto finance market includes options for nearly every credit profile. The terms, however, vary widely.

Buyers with scores above 660 access conventional lenders, credit unions, and manufacturer financing programs. These buyers qualify for the lowest rates and the most flexible loan structures. Buyers with scores between 500 and 660 typically work with near-prime or subprime lenders, who charge higher rates but still offer structured financing. Buyers below 500 often turn to buy-here-pay-here dealerships, which finance in-house at very high rates and with strict repayment terms.

A larger down payment helps buyers in every tier. It reduces the loan amount, lowers the lender’s risk, and can push a borderline application toward approval. Employment stability and a verifiable income history carry significant weight for subprime applicants, sometimes more than the score itself.

Rate shopping is a smart move, and it does not hurt your credit the way many buyers fear. Shopping for auto loan rates within a short window counts as a single inquiry and does not significantly lower your score. Credit scoring models recognize that comparing lenders is responsible behavior, not a sign of financial desperation.

For buyers with no credit history, student-focused auto loan programs exist that account for factors beyond the score, including enrollment status and co-signers.

Steps to prepare for auto loan financing:

- Pull your credit reports from Equifax, Experian, and TransUnion and dispute any errors.

- Pay down revolving credit card balances to reduce your credit utilization ratio.

- Avoid opening new credit accounts in the 90 days before applying for a car loan.

- Save for a down payment of at least 10% to strengthen your application.

- Get pre-approval with a soft inquiry to estimate your loan terms without damaging your score.

- Compare offers from at least three lenders within a two-week window to treat all inquiries as one.

- Bring proof of income, employment history, and residence to every lender meeting.

Pro Tip: Credit unions consistently offer lower auto loan rates than traditional banks for the same credit tier. If you are not already a member of one, joining before you shop can save you hundreds over the life of a loan.

How does your credit score affect the total cost of car ownership?

Credit score influence on vehicle financing extends well beyond the monthly payment. The real cost difference shows up over the full loan term, and the numbers are significant. The difference between a 5% and a 16% interest rate on a $30,000 car loan over five years can mean $10,000 more paid in interest. That $10,000 buys nothing. It is the pure cost of having a lower credit score.

Financial experts identify credit score as the primary lever controlling the total cost of vehicle ownership. A buyer with excellent credit who finances a $35,000 vehicle at 5% will pay roughly $37,300 in total over five years. A buyer with poor credit financing the same vehicle at 20% will pay closer to $47,000. Both buyers own the same car. Only the credit score separates their outcomes.

This gap affects budgeting decisions too. A buyer locked into a high rate may need to target a lower-priced vehicle to keep monthly payments manageable. That constraint limits their options on features, safety ratings, and reliability. Checking certified used car costs against your financing budget is a practical way to find value without overextending on a high-rate loan.

Key affordability facts by credit tier:

- Super prime buyers often qualify for 0% promotional financing from manufacturers.

- Subprime buyers frequently face loan terms of 60–72 months, which lowers monthly payments but increases total interest paid.

- A one-tier improvement in credit score, say from subprime to near prime, can reduce the total interest paid by thousands of dollars on a mid-range vehicle.

- Car financing with low credit score profiles often includes mandatory GPS tracking or payment assurance devices as lender conditions.

Key Takeaways

Your credit score is the primary factor lenders use to set your auto loan rate, and a single tier difference can cost or save you thousands of dollars over the life of the loan.

| Point | Details |

|---|---|

| Credit tiers drive rates | Scores above 661 unlock the best loan terms; deep subprime rates can reach 21.77%. |

| FICO Auto Score is different | Lenders use a 250–900 scale model that weights auto loan history more heavily than base scores. |

| No universal minimum exists | Subprime and buy-here-pay-here lenders serve buyers at nearly every score level, at a cost. |

| Rate shopping is safe | Comparing lenders within two weeks counts as one inquiry and protects your credit score. |

| Total cost gap is large | A rate difference of 5% versus 16% on a $30,000 loan adds roughly $10,000 in total interest. |

What I’ve learned from watching buyers ignore their credit score

Most buyers walk into a dealership focused on the car. They have a model in mind, a color preference, and a monthly payment ceiling. What they have not checked is their credit score, and that oversight costs them more than any negotiation on the sticker price could recover.

I have seen buyers with near-prime scores accept subprime loan terms because they did not know where they stood before signing. The dealership’s finance office is not obligated to find you the best rate. It is obligated to close a deal. That is a structural conflict of interest that buyers need to account for.

The FICO Auto Score distinction matters more than most buyers realize. You can have a 700 base FICO score and a noticeably lower FICO Auto Score if you have a history of missed installment payments. Walking in without knowing that gap is like negotiating blind.

My honest advice: treat your credit score as part of the car research process, not an afterthought. Check it three to six months before you plan to buy. That window gives you time to dispute errors, pay down balances, and let positive changes register. The buyers who do this consistently get better rates, better terms, and more negotiating leverage than those who show up unprepared.

Rate shopping within a two-week window is one of the most underused tools available to buyers. Most people apply once, accept the terms, and move on. Applying to three or four lenders in quick succession costs you nothing on your credit and can reveal rate differences that save you real money.

Find the right car for your credit profile with Frenzycars

Knowing your credit score is step one. Matching it to the right vehicle is step two. Frenzycars covers both sides of that decision. Whether you are working with excellent credit and want to compare top-tier models, or you are rebuilding your score and need to find the best value in a specific price range, Frenzycars has the resources to guide you. Browse best cars by category to find vehicles that fit your budget and financing profile, or check car specs by make and model to compare technical details before you commit. Buyers interested in electric vehicles can also review the best electric company cars to see how federal incentives interact with financing decisions.