TL;DR:

- A rebuilt title marks a vehicle that was declared a total loss, repaired, and passed a safety inspection. These cars pose risks like hidden structural damage, insurance challenges, and reduced resale value, which never fully go away. Buying one requires careful inspection and understanding of long-term financial and safety implications.

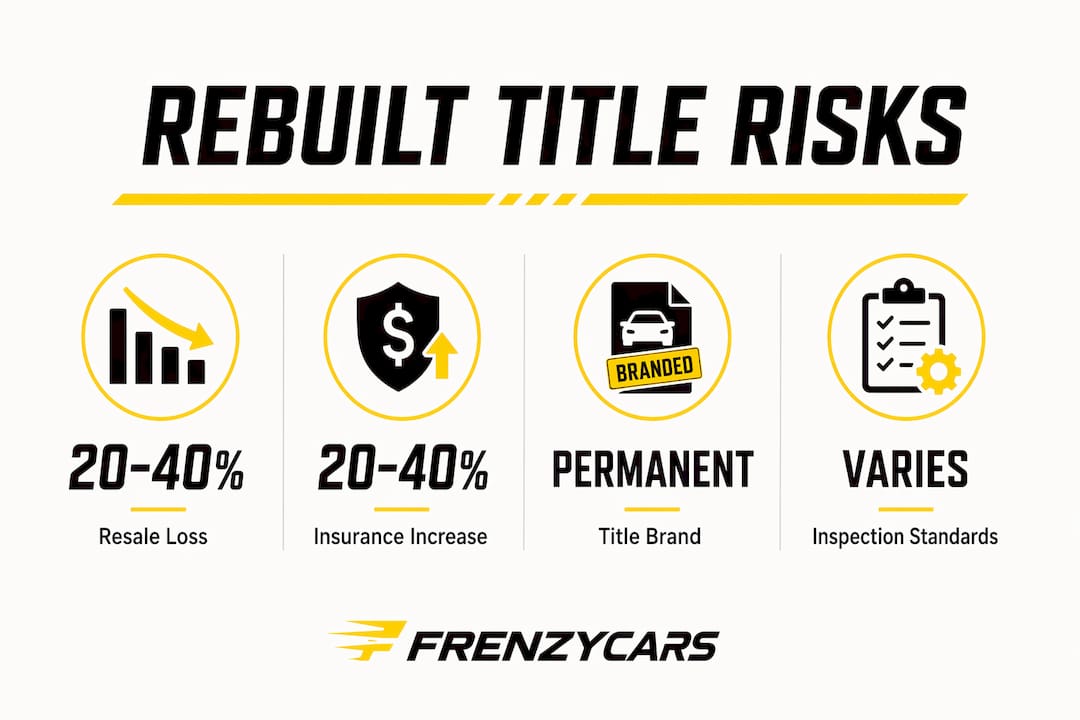

A rebuilt title is the permanent legal brand placed on a vehicle that an insurance company once declared a total loss, then repaired and passed a state safety inspection. That low sticker price is real. The risks that come with it are just as real, and they last for the entire life of the car. Rebuilt title vehicle concerns cover four major areas: hidden structural damage, insurance complications, lender restrictions, and a 20%–40% resale value drop that never goes away. Budget-conscious buyers often focus on the upfront savings and miss the long-term financial exposure. This guide breaks down every risk so you can decide with your eyes open.

Why rebuilt title cars are risky: the full picture

A rebuilt title starts as a salvage title. When an insurer decides repair costs exceed a set percentage of the car’s market value, typically 75%–80%, it declares the vehicle a total loss and issues a salvage title. The car cannot legally be driven on public roads at that point.

A repair shop or individual then fixes the vehicle and submits it for a state inspection. Pass that inspection, and the state rebrands the title from “salvage” to “rebuilt” or “rebuilt/restored,” depending on the state. The car is now road-legal again.

Here is what that process does not guarantee:

- The inspection checks minimum road safety, not long-term structural integrity.

- Repair quality varies widely because no federal standard governs the work.

- The rebuilt brand stays on the title permanently, no matter how good the repairs are.

- Disclosure rules differ by state, so private sellers are not always required to volunteer the history upfront.

One serious fraud risk compounds all of this. Title washing is a documented scheme where sellers re-register a salvage vehicle in a state with looser branding rules to erase the rebuilt designation from public records. A full VIN history check across all states is the only reliable way to catch it. The American Association of Motor Vehicle Administrators (AAMVA) recognizes title fraud as an ongoing problem in the used-car market.

Are rebuilt title cars safe? What inspections miss

State safety inspections for rebuilt vehicles focus on whether the car can operate on a road today. They do not assess whether the car will remain safe or reliable six months from now. Consumer Reports warns that buyers should avoid rebuilt titles generally because hidden electrical and frame damage routinely escapes state-level checks.

The most dangerous categories of hidden damage include:

- Frame damage: A bent or improperly repaired frame affects crash protection and handling. Modern unibody frames are especially difficult to restore to factory tolerances.

- Flood damage: Flood-related corrosion, mold, and electrical failures frequently appear months after purchase, long after the inspection passed the car.

- Airbag systems: Replaced airbags may not deploy correctly in a subsequent crash if the underlying sensors or wiring were not properly restored.

- Electrical gremlins: Modern vehicles rely on dozens of interconnected modules. Water or impact damage to one can cause cascading failures that are expensive and difficult to trace.

Manufacturers void factory warranties the moment a vehicle receives a salvage or rebuilt title. That warranty void means every repair after purchase comes entirely out of your pocket. Extended warranties exist for some rebuilt vehicles, but they carry higher premiums and significant exclusions.

Pro Tip: Before buying any rebuilt title car, hire an independent mechanic who specializes in collision repair to inspect the vehicle. A frame measurement check and a scan of all onboard diagnostic modules costs far less than discovering hidden damage after the sale.

State inspection standards also vary significantly from one state to another. Inspection requirements in some states are thorough; in others, they are minimal. A car rebuilt and inspected in a lenient state can be sold legally in a stricter state without re-inspection. Knowing which state issued the rebuilt title matters when evaluating how much the inspection actually covered. You can cross-reference a vehicle’s full history against its car specs by make and model to spot inconsistencies between reported condition and factory specifications.

How do rebuilt titles affect insurance availability and costs?

Insurance is where rebuilt title vehicle concerns become a direct financial problem. Premiums for rebuilt title cars run 20%–40% higher than equivalent clean-title vehicles. That premium increase reflects the insurer’s view that the car is a higher-risk asset with uncertain structural integrity.

The coverage restrictions are equally significant:

- Many major carriers refuse to offer comprehensive and collision coverage on rebuilt vehicles at all.

- Carriers that do offer full coverage often require a certified appraisal before binding the policy, which adds upfront cost and time.

- Gap insurance, which covers the difference between what you owe and what the car is worth if totaled, is rarely available for rebuilt vehicles.

The payout problem is the part most buyers underestimate. If a rebuilt title car is totaled in an accident, the insurer pays out based on the car’s actual cash value as a rebuilt vehicle, not as a clean-title car. Because rebuilt cars carry a 20%–40% market value discount, the payout is lower than what you might expect. If you financed the car and still owe money, that gap between the payout and the loan balance falls entirely on you.

Confirming insurance availability before signing any purchase agreement is non-negotiable. Call at least three carriers with the VIN in hand and ask specifically about comprehensive, collision, and gap coverage. For a broader look at how vehicle history affects your coverage options, the Frenzycars insurance hub covers the key factors insurers use to price rebuilt and branded-title vehicles.

What financing challenges do rebuilt title cars present?

Financing a rebuilt title car is harder than most buyers expect. Most major banks decline rebuilt title auto loans outright. The valuation uncertainty makes the car a poor collateral asset in the lender’s view, and the risk of a low insurance payout compounds that concern.

Buyers who do find financing face these constraints:

- Lower loan-to-value ratios: Lenders who accept rebuilt titles typically cap loans at 70%–75% of the vehicle’s appraised value, requiring a larger down payment from day one.

- Higher interest rates: Credit unions offer more flexibility than traditional banks but still charge higher rates and impose stricter loan amount caps than they would for a clean-title car.

- Shorter loan terms: Lenders reduce their exposure by shortening repayment windows, which raises monthly payments.

- Personal loan fallback: Buyers who cannot find an auto loan often resort to unsecured personal loans, which carry even higher interest rates and no vehicle-specific protections.

A 75% LTV cap has a concrete effect on your budget. If the appraised value of a rebuilt car is $15,000, the lender finances a maximum of $11,250. You cover the remaining $3,750 plus any fees before driving off the lot. First-time buyers who planned to put down 10% will need to recalculate entirely. Honest disclosure of the rebuilt title to every lender you approach is legally required in most states and practically necessary to avoid loan fraud complications later.

How does a rebuilt title affect resale value and your exit options?

The resale impact of a rebuilt title is permanent and significant. Rebuilt title vehicles lose 20%–40% of their market value compared to identical clean-title cars, and that discount does not shrink over time. The rebuilt brand stays on the title for the life of the vehicle, regardless of how well it was repaired or how many subsequent owners it has had.

| Ownership factor | Clean-title car | Rebuilt title car |

|---|---|---|

| Resale value | Full market rate | 20%–40% below market |

| Dealership trade-in | Standard offers | Often refused outright |

| Buyer pool | Broad | Significantly smaller |

| Title brand duration | None | Permanent |

| Long-term depreciation | Standard curve | Steeper, faster |

Many dealerships refuse rebuilt cars at trade-in entirely. Those that do accept them offer prices well below what private-party sales might yield. The private buyer pool is also smaller because informed buyers avoid rebuilt titles, and platforms that display vehicle history reports make the title status immediately visible. For buyers who plan to sell or trade within a few years, a rebuilt title car is a poor choice. The trade-in value dynamics for branded-title vehicles are consistently worse than standard depreciation curves suggest.

The one scenario where a rebuilt title car makes financial sense is long-term ownership with no plans to sell. If you buy the car outright, pay cash, confirm insurance coverage before purchase, and plan to drive it until it stops running, the upfront savings can hold. That scenario requires no financing, no near-term resale, and a thorough pre-purchase inspection by a qualified mechanic.

Key Takeaways

Rebuilt title cars carry permanent financial and safety risks that consistently outweigh their lower purchase price for buyers who need financing, resale flexibility, or reliable insurance coverage.

| Point | Details |

|---|---|

| Permanent title brand | The rebuilt designation stays on the vehicle for life, reducing its buyer pool and market value forever. |

| Insurance complications | Premiums run 20%–40% higher, and many carriers refuse comprehensive or collision coverage entirely. |

| Financing restrictions | Most major banks decline rebuilt title loans; available financing caps at 70%–75% LTV with higher rates. |

| Hidden damage risk | State inspections check road legality only, not structural integrity, leaving frame and flood damage undetected. |

| Resale value loss | Rebuilt title cars sell for 20%–40% less than clean-title equivalents, with trade-in often refused outright. |

What I’ve learned from years of watching buyers get burned by rebuilt titles

I have seen the rebuilt title conversation play out the same way dozens of times. A buyer finds a car that looks great, runs fine on a test drive, and costs $6,000 less than the clean-title equivalent. They assume the state inspection means the car is safe. They assume insurance will be straightforward. They assume they can sell it in three years without a problem. Every one of those assumptions is wrong.

The inspection tells you the car was roadworthy on one specific day. It says nothing about the frame tolerances, the corrosion inside the door panels, or the airbag control module that was reset rather than replaced. I have watched buyers discover flood damage six months after purchase when the dashboard electronics started failing in sequence.

My honest advice: run a full VIN history check through a reputable service before you even schedule a test drive. If the report shows flood, fire, or rollover damage, walk away regardless of how good the car looks. If you still want to proceed, pay for an independent inspection from a body shop that does collision repair, not just a general mechanic. They know what a properly repaired frame looks like and what a patched one looks like.

Rebuilt title cars are not automatically bad purchases. They are purchases that require more work, more verification, and more financial cushion than most first-time buyers have. If you are shopping on a tight budget and need financing, a certified pre-owned vehicle almost always delivers better long-term value than a rebuilt title car at a lower sticker price.

Smarter car research starts at Frenzycars

Frenzycars publishes detailed car specs by make and model so you can compare factory specifications against what a seller claims about a rebuilt vehicle. When a car’s reported condition does not match its original build data, that gap is a red flag worth investigating before you commit. Frenzycars also covers financing realities for different buyer profiles and ranks vehicles by category so budget-conscious buyers can find safe, affordable options without the complications that come with branded titles. Browse the best cars by category to find clean-title picks that fit your budget and driving needs without the hidden costs.